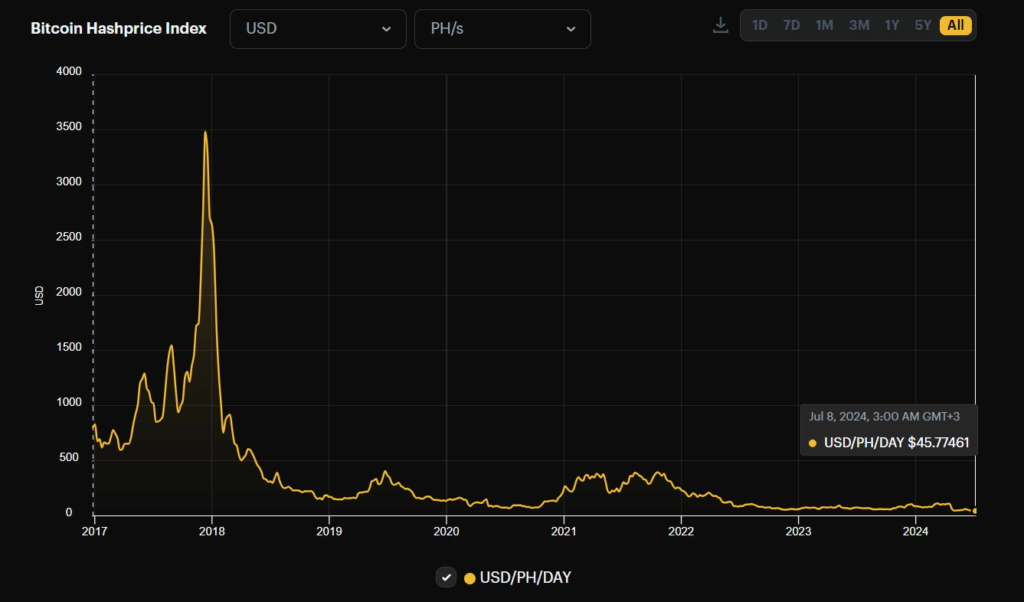

Bitcoin’s price drop last week, exacerbated by German government transfers, pushed hashprice to an all-time low of $44.31/PH/day, despite a 5% downward difficulty adjustment.

Last week’s Bitcoin (BTC) price drop, worsened by German government liquidations, had pushed hashprice, a metric that represents the miner revenue on a per terahash basis, to an all-time low. This situation is reminiscent of the summer of 2021, when China’s Bitcoin mining ban caused similar disruptions in the crypto’s mining ecosystem.

As per data from crypto mining analytics firm Hashrate Index, last week hashprice plunged to $44.31 per petahash per day (PH/day), the lowest seen in the crypto market so far. Even in May 2021, when Chinese authorities cracked down on crypto mining and trading, hashprice only fell from 379 PH/day to 203 PH/day.

Transaction fees on the Bitcoin network have also nosedived, with volumes reaching their lowest point since Q3 2023.

On July 8, the Bitcoin blockchain processed just 12.32 BTC in transaction fees, marking the lowest level in nearly nine months. Colin Harper, head of research at Luxor Technology, noted that the last time transaction fees were this low was in October 2023, when they hit 11.4 BTC amid Bitcoin’s 28.5% price surge. Hashrate Index says heatwaves could further exacerbate the stagnation in Bitcoin’s hashrate as the U.S. enters its hottest period of the year.

“For Q3-2024, changes to Bitcoin’s hashrate will result from a constant tug-of-war between heat-related curtailment, hashprice volatility, and miners deploying new ASICs.”

Colin Harper

The current landscape of consecutive negative difficulty adjustments — three in a row — mirrors that of the summer of 2021. That period was marked by turbulence due to China’s crackdown on Bitcoin mining and trading. This year, the downturn follows a tumultuous summer for Bitcoin’s hashrate in the aftermath of the fourth halving, which caused Bitcoin’s hashrate to drop by 10%.