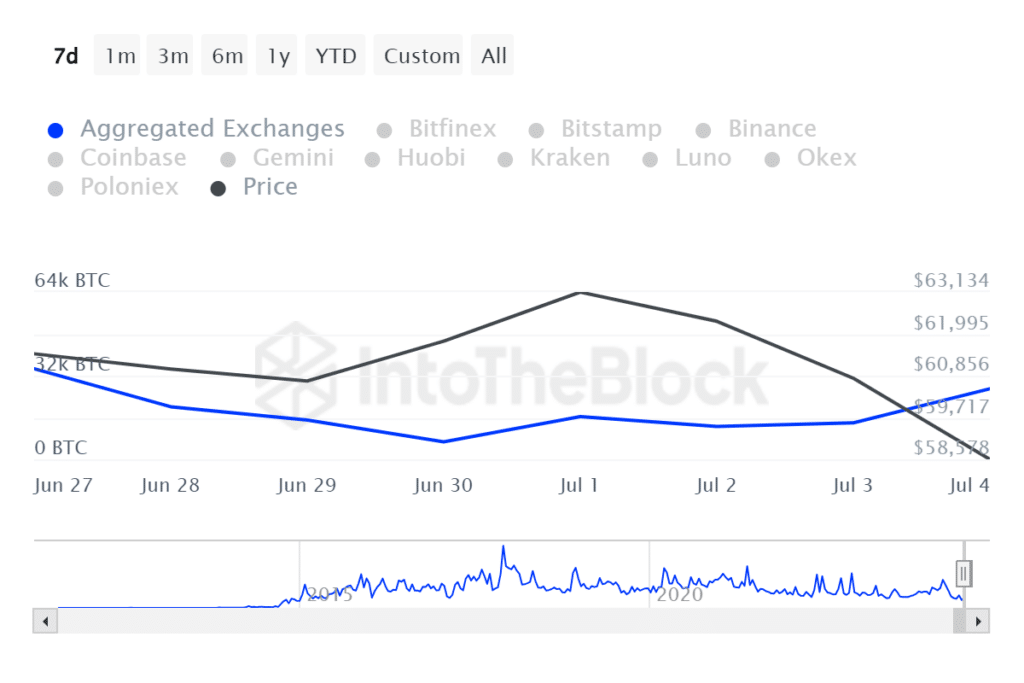

Sustained selling pressure gripped Bitcoin as exchange deposits increased due to bearish market sentiment.

According to IntoTheBlock data, crypto holders have sent over 21,000 Bitcoin (BTC) to centralized exchanges like Binance and Coinbase in the past week. The total amount of BTC transferred to these trading venues exceeded an estimated $1.2 billion.

Bitcoin’s 21% decline in the past month indicates sustained selling pressure due to macroeconomic factors, institutional capitulation, government sales, creditor repayments, and market uncertainty.

Inflation data in the U.S. showed signs of slowing down, but not enough to trigger interest rate cuts from the Federal Reserve. The central bank maintained its tighter monetary policies, reducing risk appetite as the Fed holds out for its 2% inflation target.

Following the halving, which slashed block rewards by 50%, some miners liquidated millions in crypto to finance business expenses. This trend may have slowed even as BTC remained below its $73,000 peak in March and continued a sideways or downward pattern since April. However, mining stocks took a beating during the last dip.

Spot BTC ETF flows have also stagnated, and trading volumes for BTC-backed products on Wall Street have mirrored price movements, as ETF expert James Seyffart noted.

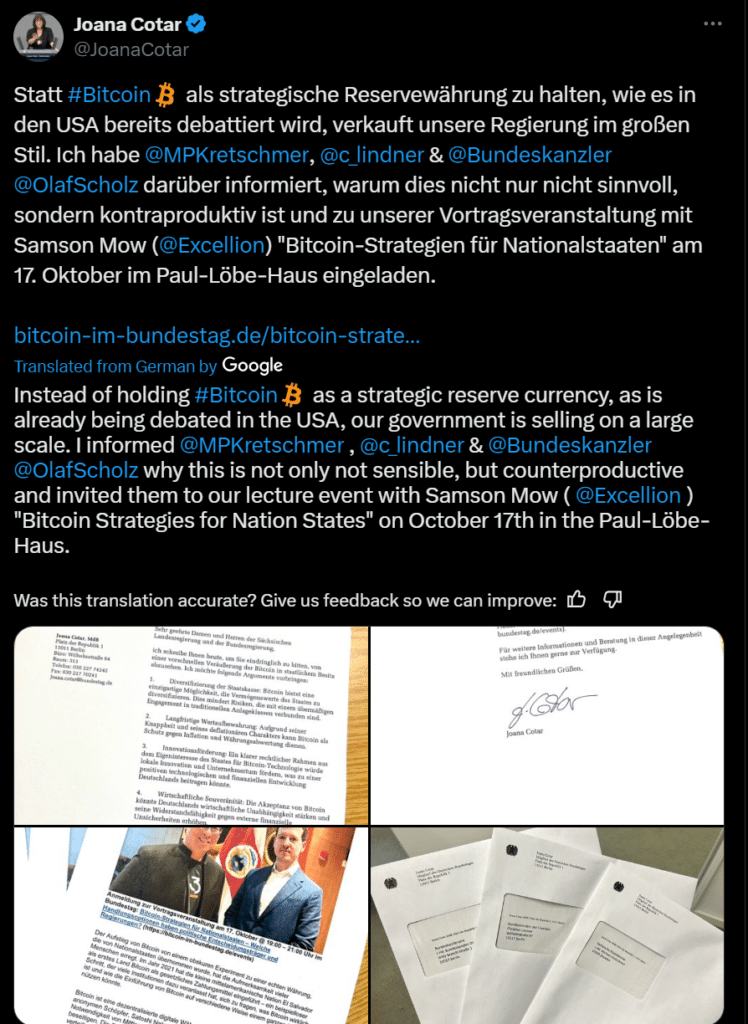

Meanwhile, authorities in Germany and the U.S. have sent thousands of Bitcoin to exchanges in the last two weeks. At least one German lawmaker has criticized the government’s BTC sell-offs. U.S. officials moved $240 million of seized Silk Road BTC to Coinbase, typically to sell in open markets.

The total cryptocurrency market is on a widespread downswing led by Bitcoin’s decline. Per IntoTheBlock, the digital asset industry lost 8% in 24 hours and dropped to $2 trillion, a five-month low. However, cryptocurrencies have collectively surged 24% and 73% in six months and over the last year, respectively.